6% is the floor for the lucky few in today’s market. Borrowers with very good to excellent credit, specifically those with a score of 740 and up, can generally expect the best rates, starting around that 6% mark, according to Forbes Advisor’s recent data. If your credit score isn’t quite in that elite tier, don’t panic. The math simply shifts.

The personal loan market has become a fragmented beast. It is no longer just about walking into a local branch and talking to a loan officer who knows your name. Now, it is a digital race. You have lenders like SoFi, Upgrade, and Discover fighting for your business through algorithms and instant approvals.

Navigating this can feel like walking through a hall of mirrors. One minute you are looking at a low APR, and the next, you realize that the “total cost of credit” includes fees that change the math entirely. It is easy to get lost in the jargon.

Deciphering the Rate Gap

The difference between a good rate and a bad rate is the difference between a manageable monthly payment and a financial sinkhole. When people look for financing, they often focus on the monthly payment first. That is a mistake. You need to look at the APR.

The APR includes the interest rate plus any prepaid finance charges. If a lender offers a low interest rate but charges a 5% origination fee, that “cheap” loan is actually quite expensive. You have to calculate how that fee impacts your long-term cost.

Credit scores act as the gatekeepers. A score of 740 might get you into the 6% to 8% range. But if your score slips into the 600s, that rate might jump to 15% or 20% almost instantly. This is why shopping around is not just a suggestion; it is a necessity.

Many people find that Bankrate’s personal loan marketplace helps them see these variations before they commit. It allows you to get prequalified, which means you can see what you might qualify for without a hard inquiry on your credit report.

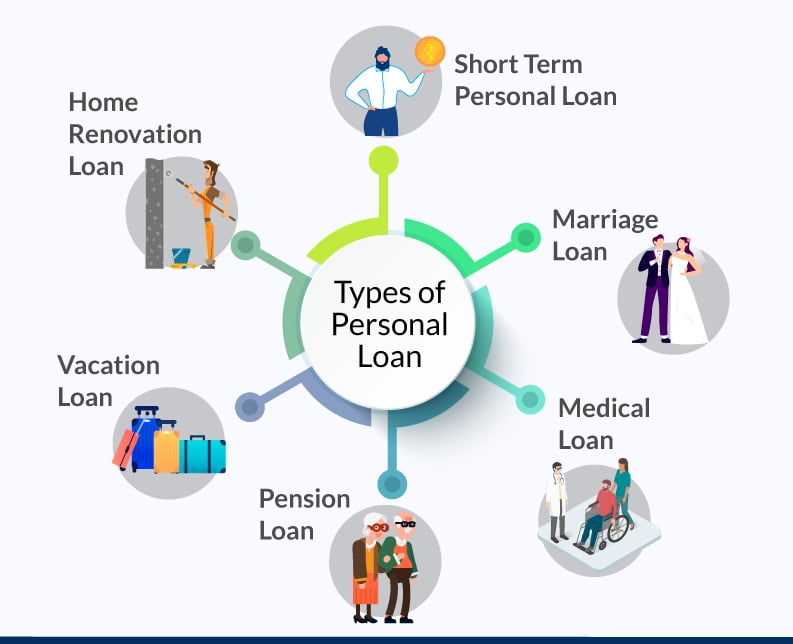

But what happens if you need money urgently for a wedding or a sudden medical bill? This is where the distinction between a personal loan and a payday loan becomes vital.

| Loan Type | Typical APR Range | Best For… |

|---|---|---|

| Unsecured Personal Loan | 6% – 36% | Debt consolidation, large purchases |

| Secured Loan | 5% – 25% | Borrowers with lower credit scores |

| Payday Loan | Often 300% – 500%+ | Emergency cash (very high risk) |

The Debt Consolidation Trap

Debt consolidation is the biggest driver of personal loan volume. The idea is simple: take out one large loan with a lower interest rate to pay off several high-interest credit cards. If you are paying 24% on a Visa card and you get a personal loan at 12%, you win. It is math in your favor.

However, there is a psychological trap here. People often pay off their credit cards with a loan, feel a sense of relief, and then proceed to run the credit card balances up again. Suddenly, they have the personal loan payment *and* the new credit card debt.

This is how a “financial solution” becomes a debt spiral. You must treat the loan as a tool to change behavior, not just a way to move numbers around on a screen. If you do not address the spending habits that caused the debt, the loan is just a temporary bandage on a much deeper wound.

Is a loan actually helping you if it extends your repayment period from two years to five years? It might lower your monthly payment, but you will end up paying significantly more in total interest over the life of that loan. You have to run the numbers on the total cost, not just the monthly slice.

For those looking for specific products, NerdWallet offers comparisons between major lenders like SoFi and Discover. It helps you see how the terms differ between a traditional bank and a fintech company.

Comparing Lenders and Loan Types

Not all money is created equal. When you go looking for funds, you might encounter a variety of structures. A business loan is not a personal loan, and a student loan has different tax implications. You need to know which bucket you are playing in before you sign anything.

Some lenders offer “fixed-rate” loans. This means your payment stays the same for the entire duration. This is great for budgeting. Other lenders might offer “variable-rate” loans. These start lower but can climb if the Federal Reserve decides to hike interest rates.

If you are an entrepreneur, a business loan might be the right move, but it often requires more documentation and collateral. Personal loans are much faster. You can often get funding within 24 to 48 hours if you have your paperwork in order.

- Personal Loans: Unsecured, fast, used for anything from home repair to weddings.

- Business Loans: Often require proof of revenue, used for scaling or inventory.

- Home Equity Loans: Use your house as collateral; lower rates but higher risk to your property.

- Student Loans: Specific to education; often have deferment and forgiveness options.

If you are in a pinch, you might see ads for fast funding through payday loans. Be extremely careful. While the speed is impressive, the cost can be predatory. These are meant for a single pay period, not for long-term financing.

Hidden Costs in the Fine Print

The “sticker price” of a loan is rarely the final price. You have to look for the fine print regarding origination fees. This is a one-time fee taken out of your loan proceeds. If you borrow $10,000 but the lender takes a 5% origination fee, you only get $9,500 in your bank account, but you still owe interest on the full $10,000.

Another thing to check is the prepayment penalty. Some lenders want to make sure they get their interest. If you decide to pay the loan off early to save money, they might charge you a fee for doing so. This feels counterintuitive, but it is a real thing that exists in certain contracts.

Then there is the matter of the “prepayment” vs. “early payoff.” Always ask specifically: “Is there a penalty if I pay this off in full next year?” If the answer is yes, you should probably look elsewhere.

Many people find that myFICO provides offers that allow them to compare these specific terms. It helps take the guesswork out of the comparison process.

And then there is the credit score impact. Every time you apply for a loan, a “hard pull” occurs on your credit report. This can cause a small, temporary dip in your score. If you are planning to buy a house or a car in the next few months, avoid applying for personal loans in the meantime. You want your credit profile to be as clean and stable as possible when you go for the big-ticket items.

Finder’s guide to loans suggests looking at the total cost of borrowing rather than just the monthly minimum. This is the single most important metric for your long-term wealth.

Before you sign any loan agreement, check the exact total amount you will have paid back by the end of the term.

Brand Anchors covers this in more detail.

FAQ

What is the difference between a personal loan and a line of credit?

A personal loan provides a lump sum of cash upfront with a fixed repayment schedule, while a line of credit allows you to draw funds as needed up to a specific limit.

How does my credit score affect my loan interest rate?

A higher credit score indicates lower risk to lenders, typically resulting in lower interest rates and better loan terms.

What are the common requirements for qualifying for a personal loan?

Lenders generally require proof of steady income, a stable residential history, and a minimum credit score to ensure repayment ability.

Can I use a personal loan to consolidate debt?

Yes, personal loans are frequently used for debt consolidation to combine multiple high-interest debts into a single monthly payment with a lower interest rate.

Are there penalties for paying off a loan early?

Some lenders charge prepayment penalties to compensate for lost interest, so always check your loan agreement for an early repayment clause.